Lets talk on the differences between a charge card and a credit card. When it comes to comparing a charge card and a credit card, they may be similar in making purchases after payment. However, there are some important differences between charge cards and credit cards, mainly in payment methods and credit.

As per credit expert John Ulzheimer, a charge card is a good option if you always pay your credit in full and on time every month. With charge cards, you do a check at the end of each month and have limited flexibility in growing your repayment period. This feature helps as a means to stop collecting the due payments.

On the other hand, a credit card would be a good choice if you have a due payment from month to month. If you understand your budget and finance allows you to make regular payments and slowly pay off your credit card. It’s important to know what is the difference between a charge card and a credit card based on your lifestyle.

Lets know more on charge card vs credit card.

What Is The Difference Between A Charge Cards And A Credit Card? Charge card vs. credit card

| Features | Charge cards | Credit cards |

| Limit of credit card | No such limit, but spending should be limited | Yes |

| Rate of interest | No available APR as dues needs to be paid in full every month | Both variable and fixed APR |

| Late fees charges | Yes | Yes |

| Annual fees | Not fix, depends on the card | Not fix, depends on the card |

| Rewards and benefits | rewards, bonus and other benefits are included | rewards, bonus and other benefits are included |

| Accessibility | Only a few options are there; and also approval requirements are hard | A number of options are there. It depends on the creditworthiness to qualify. |

| Credit score needed | Good to excellent | All ranges of credit are available |

When it comes to comparing charge cards and credit cards, the main difference lies in the capacity to keep a balance.

Charge cards generally require full payment of the balance each month, whereas credit cards allow users to have a balance with interest charges.

Now, let’s know the other important differences to know when knowing charges and credit cards.

Credit Limit

Credit cards come with a preset credit limit the issuer decides during approval. This limit depends on a number of factors, like credit score, credit history, and income.

Although credit card holders can request to increase the limit, they are up to approval from the issuer.

Having a lower credit use, below 30% of the available limit, is advised to avoid negative effects on credit scores.

Whereas charge cards generally do not have a preset credit limit. Instead, the issuer has income and spending habits to choose a perfect spending limit.

It allows the limit to be changed based on credit records, payment history, and card usage, which can be good for business owners or people with higher spending requirements.

However, it’s important to remember that charge cards always have a limit, even though it’s not clearly explained.

Also, charge card users don’t need to be worried about the use of credit since no preset spending limit exists.

By understanding these differences between charge cards and credit cards, you can make a decision based on your financial needs and spending habits.

Interest Rates

When it comes to interest rates, charge cards and credit cards have differences. Here is what you should know:

Charge cards require paying off the full balance every month, so they don’t charge an annual percentage rate (APR).

However, making payments on time is important to avoid late fees or account suspension or closure. To avoid the unexpected, carefully check the terms and conditions of your charge card or credit card agreement.

However, credit cards apply a fixed or variable APR to any carried balances from one month to the next. Also, interest is charged on late payments or cash advances.

It’s important to know that even the best credit cards available today can lead to debt if not used in good hands.

The discipline required by charge cards may be appealing to people who want to maintain financial control.

However, paying off your credit card balance in full each month is a long-term financial plan.

By understanding the interest rate plans of charge cards and credit cards, you can make decisions about which option comes with your financial goals and spending habits.

Accessibility: Charge Cards vs. Credit Cards

When it comes to accessibility, charge cards may have a number of challenges for consumers. Apart from the high annual fee, the options for charge cards are limited, with American Express being the dominant issuer.

In contrast, credit cards offer a much wider range of choices. There are a number of rewards, benefits, fees, promotional offers, APRs, and other features available, making sure that cardholders can find the credit card that best matches their lifestyle.

Another factor affecting accessibility is creditworthiness. Generally, qualifying for a charge card need a good credit score, mainly around 670 or higher.

This can make it more difficult for people with less financial history to get approval for a card.

At the same time, credit cards are more suitable and available to a number of applicants, including those with bad credit or no credit history.

Moreover, people who are unable to qualify for a credit card due to poor credit may have the option to apply for a secure credit card.

Having limited options and higher creditworthiness requirements, charge cards may be less available to some consumers.

At the same time, credit cards give a number of choices and are available to people with different credit profiles, making them a more affordable option for many.

Best Savings Accounts

Late Fees and Annual Fees

Late and annual fees are important factors to know when it comes to comparing charges and credit cards. Let’s know how they differ:

Late fees on charge cards are similar to those on credit cards, but there are a few differences.

Instead of collecting interest on unpaid and due balances, charge cards mainly impose late fees on any due monthly balance. Getting too many late fees may even result in the suspension or closure of your account.

For example, the Plum Card from American Express charges a late payment fee of $39 or 1.5 per cent of the due amount (whichever is greater in both) for the first late payment.

If you miss two consecutive billing periods, the fee increases to $39 or 2.99 percent of the overdue amount (whichever is greater in both).

Most credit cards also have late payment fees like the Discover it Cash Back, which impose the price for your first late payment (a fee of around $41 may apply). Credit cards impose late fees of up to $41 for late or returned payments.

Annual Fees

If we talk about annual fees, it’s common for charge cards to have annual fees, though some business charge cards, like the Brex 30 Card, may not charge one.

Since charge cards depend less on interest payments, issuers are more to impose annual fees.

However, like credit cards, charge cards usually come with rewards programs that can help offset the membership cost through spending or other benefits.

Credit cards usually have annual fees that start from $0 to $695. Premium travel cards have higher prices but offer savings and benefits like an airport lounge and travel statement credits.

However, a number of no-annual-fee rewards card options are available that give value, including rewards for everyday spending.

Knowing the pros and cons of late fees and annual fees will help you in choosing the card type that best matches your financial needs and choices.

Rewards and Benefits: Charge Cards vs Credit Cards

When it comes to rewards and benefits, charge cards, especially those issued by American Express, offer benefits, especially for travelers.

Many charge cards give spending options that allow you to earn rewards. Some charge cards feature a 1.5 percent cash-back rate, whereas others have reward structures to specific payment terms.

On the other hand, credit cards usually offer higher reward rates and a number of benefits, especially for specific types of purchases.

The Chase Sapphire Reserve is known as one of the top travel credit cards available.

- An annual fee of $550 is applied, and cardholders enjoy a number of benefits.

- Cardholders earn 10X points on dining purchases through Chase Ultimate Rewards.

- They also earn 10X points on hotel stays and car rentals booked via Chase Ultimate Rewards.

- Additionally, cardholders earn 10X points on Lyft rides until March 2025.

- They earn 5X points on air travel booked through Ultimate Rewards.

- Cardholders earn 3X points on general travel and restaurant purchases.

- They have access to more than 1,300 airport lounges.

- Cardholders also receive up to $300 in annual statement credits for travel expenses.

- Complete travel insurance is provided.

- Cardholders can make 1:1 points transfers to Chase travel partners.

- There is a 50 percentage points increase on travel redemptions through the Chase portal.

Many more benefits are available.

Whereas charge cards offer many rewards and benefits, credit cards usually provide higher reward rates and a number of benefits, especially for specific types of spending.

After understanding and considering your spending habits and priorities will help you decide which type of card suits your needs and maximizes your reward.

Credit Score Impact: Charge Cards vs Credit Cards

Both charge cards and credit cards play an important role in making your credit history as they check and note your payment activity to the credit bureaus.

However, there are some differences in how they affect some credit score factors.

Factors like payment history and size of credit history are considered with charge cards.

Some charge cards don’t have a preset credit limit, and it’s hard for scoring models to calculate rates for these cards.

On the other hand, credit cards affect all factors contributing to your credit score, including the use of credits.

It’s important to be careful about how much credit you use when compared to your available credit limit when using credit cards.

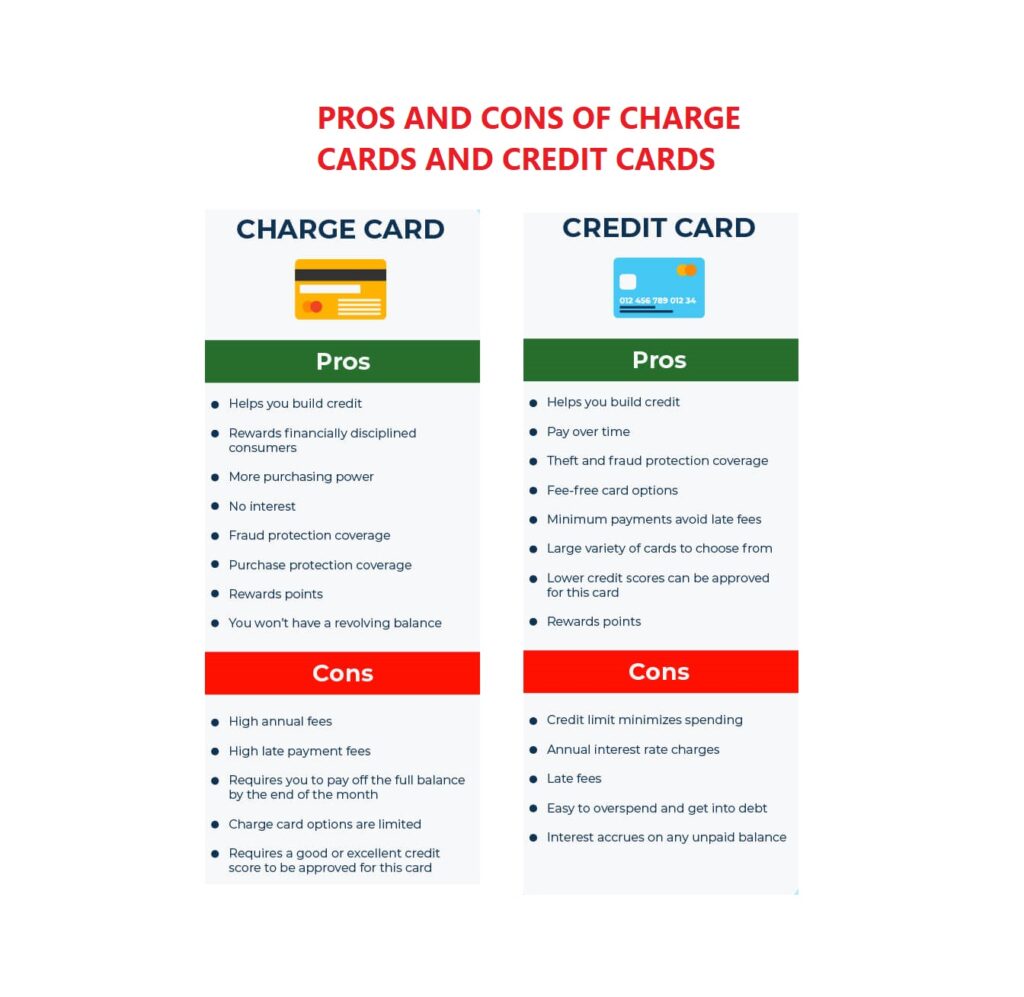

PROS AND CONS of Charge Cards and Credit Cards

Differences Between a Charge Card and a Credit Card

- Payment Method: With a charge card, you are required to pay off the full balance every month, whereas with a credit card, you have the option to carry a balance and make minimum payments.

- Credit Limit: Credit cards have a preset credit limit determined by the issuer, while charge cards typically do not have a specific spending limit. The spending limit on charge cards is determined based on income, spending habits, and creditworthiness.

- Interest Rates: Charge cards do not charge an annual percentage rate (APR) because the full balance needs to be paid off each month. Credit cards, on the other hand, charge interest on carried balances from month to month.

- Late Fees and Annual Fees: Both charge cards and credit cards can impose late fees for overdue payments. As for annual fees, charge cards are more likely to have annual fees, while credit cards may or may not have them. Annual fees vary depending on the card.

- Rewards and Benefits: Both charge cards and credit cards can offer rewards, bonuses, and other benefits. Charge cards, particularly those issued by American Express, often provide benefits for travelers. Credit cards usually offer a wider range of rewards and benefits, including higher reward rates and specific perks for certain types of spending.

- Accessibility: Charge cards generally have limited options, with American Express being the dominant issuer. Approval requirements for charge cards are typically stricter, requiring a good credit score. Credit cards, on the other hand, offer a wider range of choices and are available to people with different credit profiles.

- Credit Score Impact: Charge cards impact factors such as payment history and credit history, while credit cards impact all factors contributing to your credit score, including credit utilization.

It’s important to consider your financial needs, spending habits, and creditworthiness when choosing between a charge card and a credit card. Charge cards can provide more control over spending and may be suitable for those who can pay off their balances in full each month, while credit cards offer more flexibility but carry the risk of accumulating debt if not managed responsibly.

Conclusion

In conclusion, knowing the: difference between a charge card and a credit card, we conclude credit cards usually have more ease with credit, but they come with the risk of collecting debt if not managed by good hands. Charge cards generally require full payment each month, and loss to do so may result in account closure and late fees charges. Deciding what to choose between charge cards and credit cards depends on your financial needs and priorities, as both can help you make credit, earn rewards, and provide other benefits. Finally, the decision should be based on what best suits your financial situation and needs.

FAQs

What is a charge card?

A charge card is a payment card that works similarly to a credit card but has some crucial differences.

Unlike credit cards, charge cards require the full balance to be paid off every month, meaning you can’t carry debt from one month to the next.

Another distinction is that charge cards often don’t have a specific spending limit set in advance. Instead, your spending ability is determined by your demonstrated ability to repay.

Charge cards are commonly used by businesses and individuals with higher incomes who can afford to pay off their balances completely every month.

What is a credit card?

A credit card is a payment card that allows you to purchase and borrow money from a bank or credit card company. It provides a line of credit with a set spending limit.

You can use the card to make purchases up to that limit, and each month you receive a statement showing the amount owed.

You can pay off the full balance or make a minimum payment, with the remaining balance carrying over to the next month and accruing interest.

Credit cards offer convenience, flexibility, and sometimes rewards or perks based on the specific card.

What is better a credit card or a charge card?

Credit cards offer individuals more flexibility when managing their revolving credit, but this convenience comes with its own drawbacks.

If one carries a balance on a credit card without practicing proper discipline, one can quickly accumulate a significant amount of debt.

In contrast, charge cards operate differently as they typically require the cardholder to pay off the full balance each month, eliminating the possibility of carrying debt from month to month.

What is the benefit of charge card over credit card?

Since charge cards do not have a predetermined spending limit, credit scoring models cannot calculate the utilization ratio specifically for these cards.

This particular characteristic of charge cards offers a distinct advantage: you can spend as much as you desire within a given month without worrying about how it impacts the utilization factor of your credit scores.

What is the point of a charge card?

A charge card is a type of payment card typically utilized by businesses, and in some cases, by individuals with higher incomes. Similar to a credit card, it enables users to make purchases without immediately deducting funds from the associated business bank account.

ALSO READ: